The AI Solutions Marketplace White Paper: Market Structure, Capital Flows, and Cyberill’s Position

23 April, 2026

A white paper by Zac Buller, Corporate Development Specialist

Download “The AI Solutions Marketplace” whitepaper

The era of the isolated AI pilot is over. Not winding down. Over.

Enterprise technology is in the middle of a structural realignment, and the organizations still running disconnected proofs of concept are already behind. Deploying large language models without a governing semantic layer isn’t just inefficient — it introduces risk that most boards can’t quantify and most CISOs can’t contain.

Capital is flooding into artificial intelligence at historic velocity, but the investment thesis has changed. The market has moved past generalized chat interfaces and into autonomous agents and deep vertical solutions. That transition — from generating text to taking action — fundamentally changes the risk profile. When an AI agent can execute a trade, alter a supply chain, or modify a security policy, deterministic control becomes the gating function for enterprise adoption. Not a feature. The gating function.

At Cyberhill Partners, we believe the organizations positioned to lead the next decade are the ones that treat AI not as a software purchase, but as a strategic capability grounded in formal domain ontology. This paper unpacks the capital flows shaping the market, exposes the structural fault lines enterprises hit when they move to production, and makes the case for why ontology-driven knowledge graphs are now the mandatory control plane for secure AI operations.

Capital deployment in artificial intelligence has reached historic levels. But the narrative beneath the numbers reveals a market undergoing rapid, structural maturation. The “Model Hype” phase is behind us. The era of “Industrial Utility” has begun.

In 2025, artificial intelligence captured half of all global venture capital — roughly $211 billion. That’s an 85% surge from the $114 billion invested in 2024. Deal counts have stabilized. Deal values are shattering records. Mega-rounds exceeding $500 million jumped from 24 in 2024 to 68 in 2025 — a 183% increase.

Yet this capital remains fiercely concentrated. Twenty percent of all global VC funding in 2025 flowed into just five companies: OpenAI, xAI, Anthropic, Scale AI, and Project Prometheus. Those top five deals alone accounted for $84 billion — up 366% from the $18 billion captured by the top five in 2024.

That kind of concentration at the foundation model layer — consuming roughly 40% of total AI capital — forces the rest of the market to specialize. The remaining 60% of funding now flows into “deep vertical” AI operators and the critical infrastructure required to deploy these models securely. OpenAI’s January 2026 acquisition of Torch, aimed at building a “unified medical memory,” illustrates the aggressive downstream push. AI-native healthcare firms already report $500,000 to $1 million in ARR per full-time employee.

The enterprise response has been immediate. Enterprise AI revenue surged 208% year-over-year, scaling from $12 billion in 2024 to $37 billion in 2025. Forecasts indicate the broader enterprise AI market will expand from $24.23 billion in 2024 to over $70.91 billion by 2030, a 19.6% compound annual growth rate. Some analyses project a $155.21 billion market by the end of the decade. Verdantix estimates the enterprise AI platforms segment alone will grow from $13 billion to $50.3 billion over the same period.

For enterprise leaders, the mandate is clear. The grace period for experimentation has closed. The market demands production-grade, secure, and fully governed AI solutions.

For three years, enterprise budgets leaned heavily into experimentation. Organizations spun up isolated copilots, funded R&D playgrounds, and launched countless proofs of concept. That phase is done. A massive “composition shift” is actively reallocating budgets away from experimental pilots and directly into production-grade investments.

Moving from pilot to production forces organizations to confront the hardest structural problems in enterprise architecture: identity, data boundaries, provenance, and auditability. Overlaying advanced AI on top of fragmented, ungoverned data guarantees failure. And in those scenarios, the limitations of the underlying infrastructure get mistaken for shortcomings in the AI models themselves — a misdiagnosis that wastes cycles and erodes executive confidence.

Four trends are driving this shift and shaping enterprise demand in 2026.

Foundation models alone cannot generate enterprise value. Raw LLM capability requires deep integration and domain expertise to become useful. The major model providers recognize this. Reports indicate OpenAI and Anthropic have engaged private equity groups — including Advent, Bain Capital, Brookfield, and TPG — to establish dedicated enterprise AI consulting arms. Value has shifted decisively from the model itself to the operational application of that model within specific business contexts.

The evolution from reactive, prompt-based chat to proactive, autonomous agents represents the greatest leap in AI capability — and the greatest escalation of enterprise risk. When AI transitions from answering questions to executing live workflows, it requires strict, deterministic boundaries. Agentic behavior without a semantic control layer is a liability. An unbound “black-box” agent operating on enterprise data without an enforceable governance framework isn’t innovation. It’s negligence.

Governance is no longer a back-office compliance activity. It is the fundamental gating function for AI adoption. Making AI safe and reliable requires organizations to formalize business meanings, relationships, and constraints — and that hard requirement is driving rapid adoption of domain ontologies and knowledge graphs. Grounding AI in explicit ontologies allows enterprises to codify business logic, ensuring outputs remain accurate, governed, and secure.

The integration of knowledge graphs with AI has graduated from academic theory to mainstream enterprise architecture. Peer-reviewed research consistently demonstrates that grounding LLMs in authoritative domain ontologies dramatically improves the reliability and explainability of the resulting solutions. The market is converging on a standard stack: models paired with tools, bound together by a semantic context layer and an enforceable governance layer.

Navigating this production shift requires a clear view of how the AI solutions marketplace actually works. The ecosystem fractures into five distinct submarkets.

Cyberhill Partners sits at the intersection of governance and implementation. We provide the semantic governance layer through our proprietary ontology and knowledge graph infrastructure, and we deliver the execution expertise required to deploy it at scale.

Organizations frequently fall into the trap of buying a proprietary, compiled AI platform, assuming they can turn it on and go. They can’t. Hard-coded, rule-based software inevitably creates new data silos and severe vendor lock-in.

True enterprise AI demands a flexible, plug-and-play architecture — one where AI connects the layers of the stack dynamically rather than relying on brittle, hard-coded integrations.

A modern enterprise AI stack has five layers, and understanding them is essential to understanding what Cyberhill builds.

Most proprietary AI platforms attempt to hard-code the connections between these layers. Cyberhill takes the opposite approach. We use AI itself to dynamically bind the layers together, creating a self-healing, ever-evolving enterprise AI solution that adapts as the business changes. The result is an architecture that integrates seamlessly across all five layers — bypassing the rigidity of legacy platforms entirely.

Three enterprise AI solutions operationalize this architecture:

Cerebro functions as the semantic layer within the stack — an enterprise AI solution designed to rapidly deploy internal business AI applications. It grounds enterprise data in the governing ontology, providing the exact context and constraint required for secure operations. Cerebro deploys directly on top of existing data, in days, with zero data migration.

Wolverine is an enterprise AI solution that enables a readily deployable digital twin of anything. Currently deployed for cybersecurity — where it models threats, validates controls, and enables AI-driven, self-healing defense mechanisms — Wolverine is actively expanding into M&A due diligence, stack optimization, and a unified intelligence view for the CISO.

AIR90 (AI Roadmap 90) is our structured deployment methodology. It takes a complex business issue from raw concept to a production-ready enterprise AI solution in exactly 90 days.

As the market wakes up to the necessity of the semantic layer, the competitive landscape for ontology and knowledge graph technology has expanded rapidly. Significant confusion remains. Enterprise architects frequently conflate graph databases (the storage substrate) with knowledge graphs grounded in domain ontology (the control plane).

Understanding this distinction is critical. The vendor landscape fractures into three categories: AI workflow orchestration platforms, infrastructure hosts, and ontology foundation vendors. Many technologies that appear competitive are, in reality, complementary to Cyberhill’s architecture.

Neo4j

Neo4j is the dominant force in the graph database market, raising over $568 million at a valuation exceeding $2 billion, with an estimated $200 million in ARR. Neo4j provides a scalable graph database and serves as a backbone for GraphRAG and AI context layering, with widespread Fortune 100 adoption. Through its neosemantics (n10s) plugin, Neo4j enables RDF and vocabularies such as OWL/RDFS/SKOS, supports SHACL validation, and provides a strong developer pathway for mixing property graphs with Semantic Web standards [21] [22].

THE CYBERHILL DISTINCTION: Neo4j provides scalable graph infrastructure. Cyberhill provides the semantic governance pattern that transforms those graphs into enforceable enterprise controls. In many deployments, Cyberhill treats Neo4j (or AWS Neptune [23] [24]) as the underlying infrastructure while our ontology serves as the enterprise control-plane layer. We apply semantics as a policy-bound control and audit layer across enterprise systems, irrespective of the underlying database. The distinction is architectural: Cyberhill delivers a semantic governance fabric, not a storage engine.

Stardog

Stardog is an enterprise knowledge graph platform that unifies data based on meaning. With approximately $32.5 million in funding and estimated revenues of $13.8 million, Stardog sells a comprehensive knowledge graph and semantic AI engine — a graph store paired with reasoning and virtualization capabilities — as a software product. They offer advanced OWL-related reasoning semantics and inference features.

THE CYBERHILL DISTINCTION: Stardog is a platform vendor. Cyberhill delivers a holistic enterprise AI solution. We utilize ontology and graphs as the control plane within secure deployments, integrating directly with existing data platforms rather than forcing a rip-and-replace. Cyberhill’s approach is deployment-first: we operationalize semantics inside live enterprise workflows rather than selling a standalone reasoning engine.

Graphwise

Graphwise (formed from the merger of Semantic Web Company and Ontotext) is a comprehensive Graph AI and semantic platform. Privately held, Graphwise positions itself as a “trusted semantic backbone” for AI. They offer tooling for building and managing knowledge graphs and semantic content at scale, utilizing GraphDB as an RDF/SPARQL-compliant graph database.

THE CYBERHILL DISTINCTION: Graphwise provides the tooling to build and manage knowledge graphs. Cyberhill applies ontology specifically to enterprise security, identity, policy, and AI workflow governance. The core differentiation is our “secure operationalization” overlay — we tie semantics directly to policy enforcement in live production environments.

TopQuadrant

TopQuadrant is a legacy enterprise data governance and knowledge graph vendor with deep Fortune 1000 engagements. Their TopBraid EDG provides a strong governance suite and semantic modeling capabilities, positioning itself as an “AI-ready data foundation” for capturing conceptual models, ontologies, and policies [19] [20].

THE CYBERHILL DISTINCTION: TopQuadrant provides a data foundation layer. Cyberhill operationalizes that foundation into agent execution boundaries, cybersecurity controls, and active production workflows. TopQuadrant fits perfectly into a Cyberhill enterprise AI solution as a data layer; it does not replace the Cyberhill control plane.

Unframe

Unframe is a turnkey enterprise AI deployment platform based in Israel. Backed by $50 million from Bessemer and TLV Partners, they carry a valuation of approximately $132 million with estimated revenues of $5.5 million. Unframe utilizes a “blueprint” methodology for contextual grounding of LLMs and emphasizes rapid deployment, claiming the ability to deploy in hours.

THE CYBERHILL DISTINCTION: Unframe is a direct competitor in the deployment space. However, Cyberhill’s deep expertise in ontology provides a significantly more robust control plane for highly governed industries. Cyberhill’s semantic architecture could seamlessly integrate with platforms like Unframe, providing the underlying governance rules that their deployment engines execute.

Scale AI

Scale AI has raised over $1 billion in funding — backed by Peter Thiel’s Founders Fund — reaching a $14 billion valuation in May 2024 with estimated revenues of $870 million. Originally built on data annotation, Scale has expanded aggressively into AI infrastructure, enterprise deployment, evaluation, and risk oversight. In March 2026, Meta launched Scale Labs in partnership with Scale AI, signaling a deeper push into enterprise-grade AI tooling and model evaluation infrastructure. Scale AI is one of the five companies that captured 20% of all global VC funding in 2025, placing it squarely in the foundation-layer capital concentration described in Section 2.

THE CYBERHILL DISTINCTION: Scale AI dominates data annotation, evaluation, and model infrastructure. Cyberhill’s ontology-driven control plane is entirely complementary — providing the specific governance, identity, and policy enforcement layer that Scale AI does not address. Where Scale AI ensures models are trained and evaluated correctly, Cyberhill ensures those models operate within enforceable semantic boundaries once deployed in live enterprise environments.

Glean

Glean is an enterprise AI search company that has raised over $350 million, carrying a valuation of approximately $7.2 billion with an estimated ARR between $100 million and $200 million. Glean provides unified workplace search and generative AI assistants, positioning itself as a “system of knowledge” for enterprise productivity.

THE CYBERHILL DISTINCTION: Glean operates in the knowledge management and enterprise search space. Cyberhill doesn’t compete with Glean. Instead, Cyberhill’s ontology-driven control plane provides the governance and identity enforcement layer that broad enterprise search platforms inherently lack.

With $10 million in trailing twelve-month revenue on just $11 million in funding, Cyberhill occupies a highly capital-efficient, execution-focused tier. Our advantage isn’t built on replacing graph infrastructure. It’s built on utilizing ontology and knowledge graph semantics to enforce strict governance, identity, and policy constraints in live production environments. The competitors listed above are primarily platform vendors monetizing software distribution — a highly capital-intensive model. Cyberhill’s approach is entirely distinct. We are a deployment and secure integration leader. Our ontology and knowledge graph function as reusable intellectual property that accelerates time-to-value across every customer environment.

Every distinction made in the previous section — why Cyberhill isn’t Neo4j, why it isn’t Stardog, why it isn’t Unframe — comes back to one architectural decision: the ontology. Understanding what that means in practice, and why it’s so difficult to replicate, is the key to understanding Cyberhill’s durable advantage.

Cyberhill views ontology as the ultimate competitive moat in enterprise AI. Here’s why.

An ontology is a formal model of classes, relationships, and constraints. It defines specific entities and exactly how they relate to one another within a given domain. In enterprise AI, these ontologies are built on Semantic Web standards: RDF serves as the graph data model, OWL acts as the ontology language, and SHACL handles validation and constraint enforcement [11] [12] [13]. These standards make semantics machine-readable and strictly enforceable. They allow AI systems to use consistent meanings across disparate data silos, validate complex data structures, and generate traceable, explainable reasoning pathways.

Driven by the need to provide structured, proprietary context for Generative AI and RAG deployments, the Semantic Web and knowledge graph market is projected to surpass $7.7 billion by 2030.

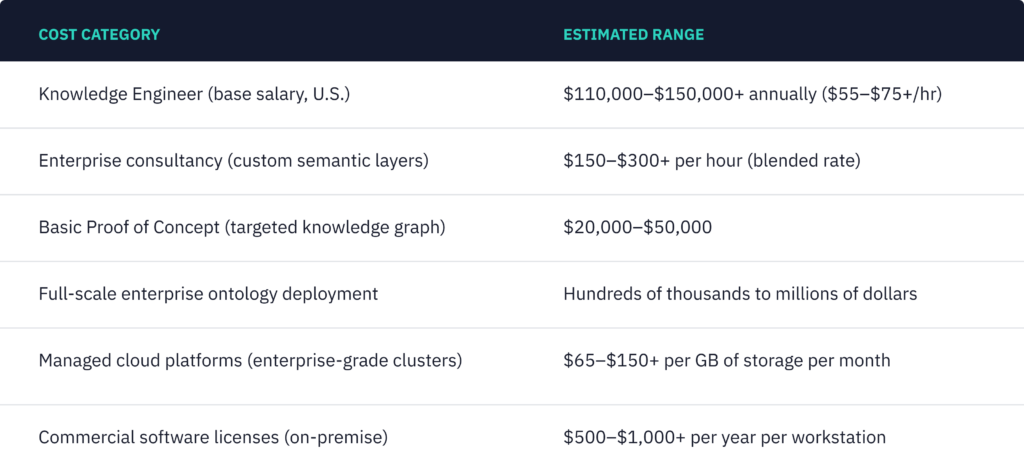

Semantic engineering expertise is exceptionally scarce. The largest cost center in the ontology market isn’t software — it’s the human capital required to build, integrate, and maintain the architecture.

Organizations attempting to construct their own ontologies face punishing financial hurdles across multiple dimensions.

Beyond direct financial outlays, organizations absorb the massive time cost of mapping relationships, resolving semantic conflicts across departments, and maintaining the ontology as the business evolves. A market for pre-trained, domain-specific ontology templates is emerging to address this gap, but proprietary vendor models carry substantial annual licensing fees. Open consortium models — including FIBO for finance and SNOMED CT for healthcare — offer a baseline, but require significant customization to become operationally viable.

Cyberhill bypasses these bottlenecks entirely. We combine open consortium ontologies, targeted third-party acquisitions, and our proprietary Ontology Scraper — a tool that constructs comprehensive ontologies in seconds. The result is a robust semantic foundation that plugs directly into any layer of the enterprise AI stack. By embedding these ontologies within a flexible architecture that supports plug-and-play integration, Cyberhill drastically accelerates time-to-production and eliminates the crippling costs of in-house development.

Every ontology Cyberhill builds becomes reusable intellectual property. When we deploy for a healthcare client, the resulting ontology — the entity definitions, relationship mappings, constraint rules — becomes the foundation for the next healthcare engagement. When we deploy for a financial services firm, the FIBO-grounded ontology we refine carries forward. The semantic model compounds with every engagement.

This is a structural advantage that no platform vendor can replicate. A software company ships a product and moves on. Cyberhill accumulates domain-specific semantic intelligence with every deployment. Over 1,000 enterprise engagements, that accumulation becomes a moat — not because it is difficult to build an ontology, but because it is nearly impossible to replicate the depth and breadth of a semantic library refined across that many real-world enterprise environments.

The Ontology Scraper accelerates the initial construction. The accumulated library accelerates every subsequent deployment. Together, they are why Cyberhill can deliver a proof point in three days and a production solution in 90 — not because we move fast, but because we have already done the hard work.

Cyberhill’s ontology organizes enterprise AI around the specific entities that dictate operational safety and compliance. We map five critical categories:

The distinction here matters: the ontology is not passive documentation. It is an active, enforceable layer. When an AI agent attempts to initiate an action, the system instantly verifies the relationships defined in the ontology. It confirms the agent is authorized to execute the workflow, verifies the workflow is governed by the correct policy, and ensures that policy permits access to the requested data. To scale this capability, Cyberhill is actively developing an Upper Ontology to provide foundational rules and standardization across all new domain deployments.

Cyberhill deploys these production-grade ontologies to drive the dynamic construction of knowledge graphs at query time. The knowledge graph serves as a live representation of enterprise entities and their relationships — functioning simultaneously as the context engine (providing structured facts), the constraint engine (ensuring actions adhere to strict boundaries), and the audit fabric (logging decisions and action chains for governance review).

This architecture directly aligns with published research proving that knowledge graphs grounded in authoritative domain ontologies significantly enhance both the reliability and explainability of LLM-based systems [4].

Two capabilities separate Cyberhill’s approach from traditional semantic databases. First, by constructing the knowledge graph dynamically on each call, Cyberhill eliminates punitive per-node pricing models and drastically reduces storage overhead. Second, Cyberhill captures and stores a Reasoning Path for every query — a timestamped, traceable, and fully auditable record of every AI decision.

This practice is rooted in a decade of mission-critical AI deployment within the U.S. Intelligence Community. As AI systems become increasingly autonomous, regulated industries will demand absolute transparency. We expect Reasoning Paths to become a mandatory regulatory requirement across all governed sectors.

As Cyberhill expands across verticals and client environments, the compounding value of the ontology depends on a shared foundation. Cyberhill is actively developing an Upper Ontology — a set of foundational rules, entity definitions, and relationship patterns that standardize the semantic layer across all new domain deployments.

The Upper Ontology is not a constraint on customization. It is the scaffold that makes customization faster. Every new vertical deployment inherits the proven structural logic of the Upper Ontology, then extends it with domain-specific entities and rules. The result is a semantic architecture that scales without starting from scratch — and one that compounds in value with every engagement Cyberhill completes.

This is the architectural foundation that makes the deployment commitments in Section 8 possible. The three-day proof point and the 90-day production timeline are not aspirational. They are the direct result of a semantic infrastructure that has been built, tested, and refined across more than 1,000 enterprise engagements.

Section 4 introduced the five-layer architecture and the three enterprise AI solutions that operationalize it. This section goes deeper — into how those solutions perform in live enterprise environments, where they are headed, and why the deployment model compounds over time.

Deploying Business AI on Existing Data

Cerebro functions as the semantic layer within the enterprise AI stack. It grounds an organization’s existing data in the governing ontology, providing the exact context and constraint required for secure AI operations — without requiring data migration. Cerebro deploys directly on top of what’s already there.

What makes Cerebro distinct is the speed of deployment and the depth of integration. Because the ontology provides a pre-built semantic scaffold, Cerebro doesn’t need months of data engineering to become operational. It connects to existing data sources, applies the ontology’s governance rules, and begins delivering AI-driven outputs in days. For organizations stuck in pilot purgatory, Cerebro is the bridge to production.

The Digital Twin That Adapts

Wolverine enables a readily deployable digital twin of anything — any stack, any domain, any environment. Its current commercial deployment is in cybersecurity, where it models threats, validates controls, and enables AI-driven, self-healing defense mechanisms. Wolverine provides the CISO with a unified intelligence view across the entire security posture.

But the architecture is domain-agnostic by design. Wolverine is actively expanding into M&A due diligence — where it maps the technology stacks of acquisition targets against governance requirements — and stack optimization, where it identifies redundancies, vulnerabilities, and integration opportunities across complex enterprise environments.

From Concept to Production in 90 Days

AIR90 (AI Roadmap 90) is Cyberhill’s structured deployment methodology. It takes a complex business issue from raw concept to a production-ready enterprise AI solution in exactly 90 days. AIR90 isn’t a sales pitch — it’s a delivery commitment backed by a repeatable process that has been refined across hundreds of engagements.

Cyberhill is actively building deep, industry-specific solutions on top of the Cerebro and Wolverine foundations. These span:

Because each vertical solution inherits the full ontology and knowledge graph infrastructure, new use cases deploy in days, not months. The ontology doesn’t start from scratch for each client — it compounds. Every engagement strengthens the underlying semantic model, which accelerates the next deployment.

When Lands’ End approached Cyberhill with a complex business challenge, we demonstrated how our ontology-driven approach could materially impact their online sales within three days. That speed isn’t an anomaly. Cyberhill routinely takes a prospective client’s business problem and delivers a working AI proof point in days — not months, not quarters.

Enterprise AI is not a one-time deployment. Data changes. Workflows evolve. Business rules shift with every acquisition, reorganization, and regulatory update. If the ontology and knowledge graph don’t evolve with them, the AI degrades — silently, and then catastrophically.

Cyberhill calls this ongoing discipline Semantic Integrity: the continuous process of keeping the ontology, knowledge graph, and deployed AI solutions aligned with the live enterprise environment. It encompasses schema updates as new data sources come online, relationship remapping as organizational structures change, constraint tuning as compliance requirements tighten, and validation that every Reasoning Path still reflects current business reality.

This is a named, differentiated service capability — not a checkbox in a platform license. Platform vendors ship software and move on. Cyberhill maintains the semantic layer as a living system, because the moment it falls out of sync with the enterprise, every AI decision built on top of it becomes unreliable. Semantic Integrity is what separates a deployment from a durable capability.

This rapid deployment capability isn’t theoretical. It’s built on a foundation of over 1,000 enterprise solutions delivered for organizations including Disney, PayPal, GAP, Levi’s, and Putnam. That track record is the proof point behind every claim in this paper — and it’s the reason Cyberhill can make deployment commitments that platform vendors cannot.

The AI solutions marketplace is expanding at breakneck speed, but the center of gravity has permanently shifted to production. Secure integration, strict governance, and durable workflows are now the decisive factors for enterprise adoption. Ontologies and knowledge graphs are no longer optional architectural enhancements. They are the foundational infrastructure required for any AI system that must be explainable, controllable, and fit for enterprise deployment.

Cyberhill Partners operates at a valuable intersection: secure enterprise AI delivery backed by a domain ontology that transforms semantic structure into an operational control plane. While ontology-first platform vendors provide the substrate, Cyberhill provides the execution — applying semantics directly to identity, policy, and production workflows, the exact areas where governance is non-negotiable and ROI depends entirely on safe deployment.

In a market with no shortage of tools but a persistent deficit of trust, ontology-driven, policy-bound delivery is a durable competitive advantage — and Cyberhill is built around it.

Ready to move from pilot to production? Cyberhill delivers a working proof point in three days.

Schedule an AI Strategy Session

Download “The AI Solutions Marketplace” whitepaper

About the Author:

Zac Buller, Corporate Development Specialist, Cyberhill Partners

Zac Buller leads corporate development at Cyberhill Partners, where he focuses on market intelligence, strategic positioning, and the commercialization of Cyberhill’s enterprise AI solutions. He works at the intersection of capital markets and enterprise technology, helping organizations understand where the AI solutions marketplace is heading and how Cyberhill’s ontology-driven approach creates durable competitive advantage.

The following table highlights recent venture capital investments in the AI ontology and semantic layer space, demonstrating the significant capital flowing into this critical infrastructure.

[1] Arizton, “Enterprise AI Market Forecast,” 2024–2030.

[2] Grand View Research, “Enterprise AI Market Report,” 2024–2030.

[3] Verdantix, “Enterprise AI Platforms Forecast,” 2024–2030.

[4] Peer-reviewed research on knowledge graphs (domain ontologies) improving reliability and explainability of LLM-based solutions.

[5] Stardog, “What is a Knowledge Graph,” positioning on reasoning, virtualization, and AI reliability.

[6] Rowspace, “$50M Launch” (press release).

[7] Union.ai, “$10M Seed Round” (press release).

[8] Union.ai, “$38.1M Series A” (coverage/announcement).

[9] Resolve AI, “$125M Series A at $1B Valuation” (press release).

[10] Loop AI, “$14M Series A” (press release).

[11] W3C, “RDF 1.1 Concepts and Abstract Syntax.”

[12] W3C, “OWL 2 Web Ontology Language Primer.”

[13] W3C, “Shapes Constraint Language (SHACL) Recommendation.”

[14] Stardog, “Enterprise Knowledge Graph Platform Positioning.”

[15] Stardog, “Documentation on Advanced Reasoning Features (OWL Semantics/Inference Behavior).”

[16] Graphwise, “Merger Announcement” (Ontotext site).

[17] Graphwise, “Merger Press Release” (PR Newswire).

[18] Ontotext, “GraphDB Product Description (RDF/SPARQL, W3C Compliance).”

[19] TopQuadrant, “TopBraid EDG as KG-Powered Data Foundation.”

[20] TopQuadrant, “TopBraid EDG Documentation: Capturing Conceptual Models, Ontologies, Policies, and Governance Assets.”

[21] Neo4j, “Neosemantics (n10s) Overview: RDF + OWL/RDFS/SKOS.”

[22] Neo4j, “Neosemantics GitHub: SHACL Validation and Ontology Import Features.”

[23] AWS, “Amazon Neptune Documentation: Gremlin, openCypher, and SPARQL for RDF.”

[24] AWS, “Amazon Neptune: SPARQL/RDF Access Patterns Overview.”